July 14 / Trade Alert For The Sigma Portfolio (Live)

Execution Date: May 13 2026 - Market Close

Email: andrei@signal-sigma.com

Follow & DM on X: @signal_sigma

We will use today's post CPI relief rally to bring our equity risk allocation back to target (60%). This implies removing around 15% from our weighting in stocks, and transferring some capital to bonds and cash.

While not an outright bearish change, this rebalancing session echoes our limited conviction for the months ahead and better aligns our portfolio with the Enterprise Strategy which now suggests caution. The focus for removal were positions excessively correlated with the Momentum Factor ETF, as well as those presenting an unfavorable risk / reward ratio.

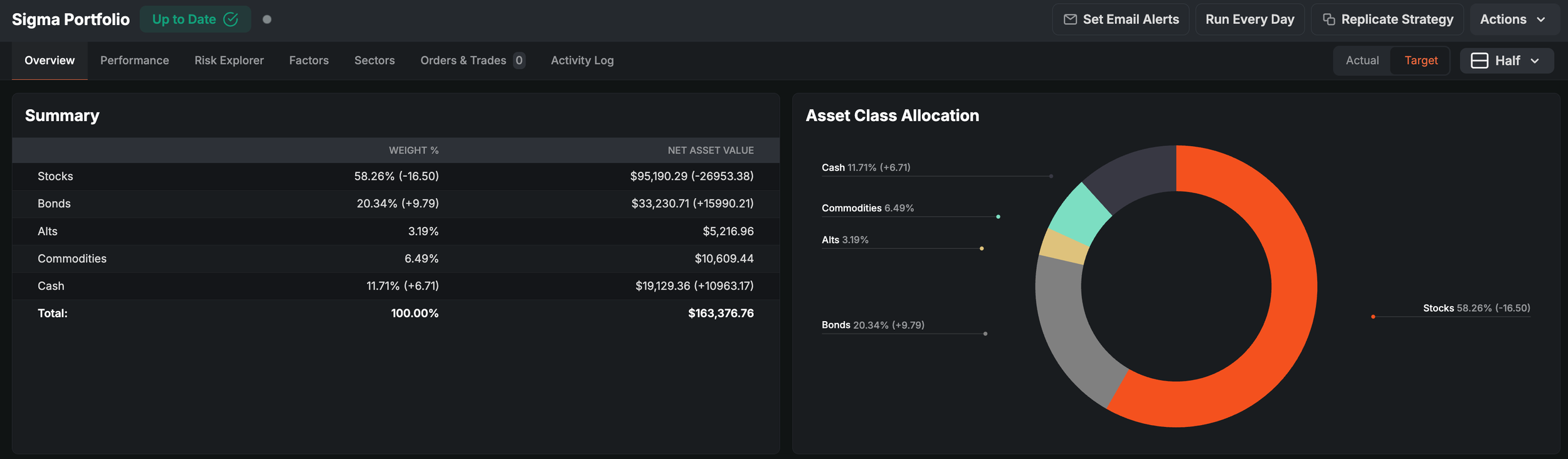

This is how our final asset class allocation will look like after today’s close:

Stocks: 75% --> 58%

Bonds: 10% --> 20%

Alternatives: 3% (unchanged)

Commodities: 6% (unchanged)

Cash: 5% --> 11%

This is the basket of trades which will be executed at today's close:

Sell to Close (sold the entire position)

SELL GTX (Close Position)

SELL VIRT (Close Position)

SELL SITM (Close Position)

SELL KLAC (Close Position)

SELL AGX (Close Position)

SELL TTMI (Close Position)

SELL CAT (Close Position)

SELL FICO (Close Position)

SELL FLNC (Close Position)

Trim (reduced existing position)

SELL LLY (Trim ~0.75% from Position)

SELL NTAP (Trim ~0.68% from Position)

SELL FIX (Trim ~1.16% from Position)

SELL MRNA (Trim ~0.92% from Position)

SELL CRS (Trim ~0.75% from Position)

Initiate (add new position)

BUY IEF (Initiate New Position — Add ~10.44%)

BUY CF (Initiate New Position — Add ~4.68%)

BUY GWW (Initiate New Position — Add ~4.46%)

As always,

Happy investing,