/ December 02 / Weekly Preview

-

Tuesday:

ISM Manufacturing PMI (48.6 exp.)

---

Wednesday:

N/A

---

Thursday:

ISM Services PMI (52.1 exp.)

---

Friday:

Core PCE Price Index MoM (0.2% exp.)

Michigan Consumer Sentiment Prel (52 exp.)

Personal Income MoM (0.4% exp.)

Personal Spending MoM (0.4% exp.)

-

Tuesday:

BHP Group Limited

CrowdStrike Holdings, Inc.

---

Wednesday:

Salesforce, Inc.

Royal Bank Of Canada

Snowflake Inc.

UiPath, Inc.

---

Thursday:

Toronto Dominion Bank (The)

Bank Of Montreal

Ulta Beauty, Inc.

Dollar General Corporation

---

Friday:

Victorias Secret & Co.

Seasonality Kicking In

Got a question about the markets, your investments, or a topic you’d like us to discuss in an upcoming article? We read every message and may feature your question in our daily write-ups!

Email: andrei@signal-sigma.com

Follow & DM on X: @signal_sigma

Last week, markets surged right into the Thanksgiving holiday, ending the short trading week with substantial gains across all major U.S. indexes. The S&P 500 rose +3.7%, rebounding strongly from short-term oversold conditions as retail traders stepped in to buy-the-dip.

Besides “the dip” providing an entry point opportunity, the main catalyst were falling bond yields and an increasing perception that the Fed is due for another round of easing in December. Currently, prediction markets are pricing in a 90% chance of a rate cut at the December meeting next week.

Real-time inflation data continues to trend sideways for the month (and lower for the year). In this context, lower bond yields are acting as a tailwind to equity prices, as investors are starting to price in stronger earnings and economic growth in 2026.

Despite talks of A.I. being in a bubble, it was precisely tech and A.I.-related stocks which led the markets higher over the last week. Mega-caps also lifted the Nasdaq, as narratives surrounding NVDA’s earnings beat managed to reinforce yje bull case around Tech.

“Magnificent Seven” leadership also contributed to outsized returns at the index level, though participation was no so great in the broad market.

Heading into December, all eyes turn to the upcoming PCE inflation report, jobs data, and the final round of Fed comments before the blackout period. Momentum and seasonality favors the bulls, despite some fragile foundations and persistent concerns.

In the technical sense, markets managed to clear resistance at the 50-DMA and M-Trend levels, rebounding from the prior AI- and rate-cut-wobble selloff. Though the late October highs were not recaptured, the benchmark equity ETF is also not overbought at the moment. Buying in Dark Pools was substantial and GEX is positive on all time-frames, lending credibility to a potential rally set-up in December.

Support stands at $669 (50-DMA & M-Trend), with resistance now at $706 (R1). It’s worth pointing out that the overall channel slope for SPY now has a less pronounced CAGR than at the start of the year, moving from 22% to 19%. As such, support and resistance levels will start to compress, barring any more significant gains. The uptrend remains intact, with the bounce from speculative excess putting prices back into the upper half of the trading channel.

Seasonally speaking, the current gain of +1.77% since October is underwhelming, given prior historical performance in Q4. On a bigger picture basis, the index remains up around 16% year-to-date, reflecting increased investor confidence, tempered with a period of digestion and consolidation of recent gains — which is totally normal.

If seasonal patterns play out (December being one of the best months for equity returns), the path of least resistance is higher into year-end.

Volatility has cooled, though it still exists. The “panic-bid” for protection has faded out after the previous spike (lower panel represents 1-Month premium for SPY options). This is consistent with a market transitioning from a “shot across the bow” correction to a more typical year-end positioning grind. At the moment, we view options as relatively cheap, from an IV standpoint.

Breadth has improved, but there are still issues. We track several metrics in this sense. The number of stocks trading above key averages is now back at more normal levels, with around 60% of stocks in the market trading above both their respective 50 and the 200 DMAs.

Topping pattern breadth has greatly improved, with the number of stocks in problematic setups dropping below the alert threshold (though we would like to see this metric continue to come down meaningfully).

As it stands, we would call this a solid improvement that sits just short of being labeled a full “buying regime”, especially since the green light is lacking on the GEX and MACD study (lower chart).

The bullish case heading into December hinges on the Fed’s dovishness and greater participation from most stocks, to set up a positive start of 2026. Left to its own devices, the market should drift higher, especially since stock buybacks will put a floor under prices.

There are still under-invested professional managers prone to chasing any rally this month if technical resistance gives way. AI leaders and other higher risk assets (like bitcoin) are favored in this scenario.

The bearish case is that valuations come into the spotlight again, as bears like to highlight. Breadth is not where it should be in a continued rally. The Fed could sound hawkish on the next FOMC meeting, case in which high risk areas of the market will suffer.

There is also the wildcard of delayed economic releases (due to the government shutdown) which could shake things up if weaker than expected data is published all at once.

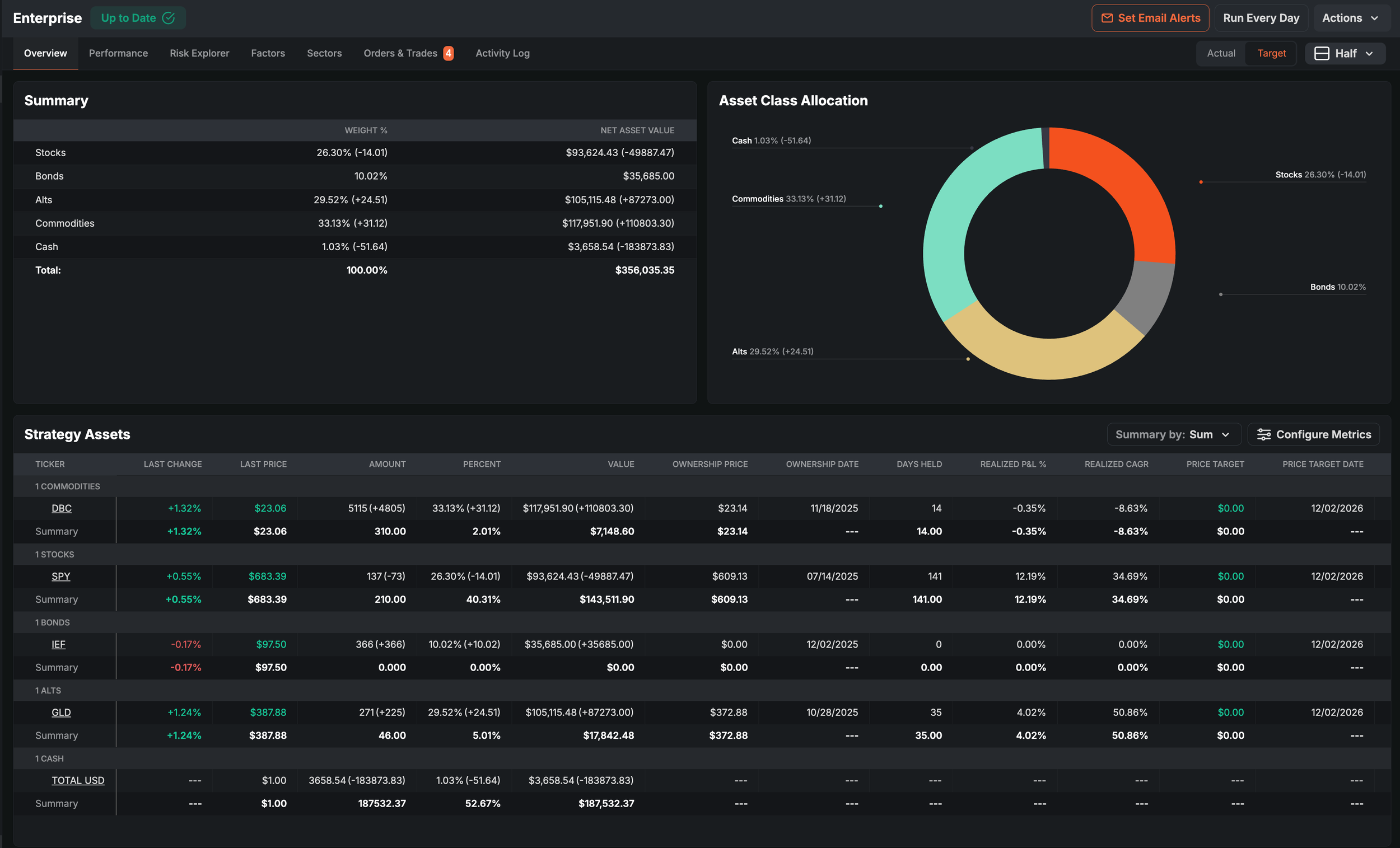

Enterprise, our primary allocation model, is rebalancing positions today into a maximally diversified asset class mix. Stocks, Gold and Commodities hold nearly similar weighting in the model, with bonds coming in last and cash being non-existent. While relatively risk-on due to the absence of cash, the model is sending a warning that going full bore on risk is not the solution at the moment.

Next week will be pivotal for investors, with the Fed meeting taking center stage amid thin liquidity and delayed data releases. This week will see traders position ahead of the event, with the potential to reinforce or derail the traditionally bullish year-end setup.

A few strong prints — on inflation, employment, manufacturing, or services — could validate a bullish year-end narrative. Conversely, any surprise weakness could deflate current optimism. Inflation data is especially sensitive, and the upcoming PCE release is expected to shape market expectations ahead of the next DOMC meeting on December 9–10. Surprises, either good or bad, have the potential to move markets significantly more than usual.

Fundamentally, while expectations heading into Q3 were low, most of the bearish concerns have been laid to rest. Over 75% of companies beat estimates, 74% beat revenues, and 61% beat on both in Q3 Earnings Season. More importantly, profit margins did not collapse, which was the main tariff-related fear.

Forward guidance, while cautious, remained optimistic. That helped reset sentiment and reduce fears of an imminent earnings recession.

Our Trading Strategy

With primary uptrends intact and a healthy (if uneven) rebound, markets are set up for continued gains going forward. While there are undoubtedly many concerns heading into 2026 that investors should be aware of, over the next few weeks, several catalysts suggest that the “pain trade” is likely to be higher.

One of the more important points is that selling appears to have run its course. Forced de-risking is no longer a factor at the moment, providing the necessary fuel for sustained upside. This is especially true with Tech shares, where selling volume has subsided to a normal range, from previous extremes. Now, with earnings season mostly complete, blackout periods ended, and companies (particularly the mega-caps) stepping back in as steady buyers of their own stock — the backdrop for a year-end rally has improved.

Nothing is guaranteed in this market, but our read is that professional traders have shifted neutral or net-long for the remainder of 2025. As such, the near-term outlook is constructive.

Signal Sigma Research & PRO members will be notified by Trade Alert of any live portfolio changes (if subscribed). If you’re not on this plan yet, you can get a free trial when you join our Society Forum. If you need any help with your trading strategy (or would like to implement one on your account), feel free to reach out!

Disclosures / Disclaimers: This is not a solicitation to buy, sell, or otherwise transact any stock or its derivatives. Nor should it be construed as an endorsement of any particular investment or opinion of the stock’s current or future price. To be clear, I do not encourage or recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the facts or perceived implications of this blog post. I currently do not own or plan to own any position, long or short, in the securities mentioned.

I am not a financial advisor licensed in the United States. Nor am I providing any recommendations, price targets, or opinions about valuation regarding the companies discussed herein. Any disclosures regarding my holdings are true as of the time this article is written, but subject to change without notice. I frequently trade my positions, often on an intraday basis. Thus, it is possible that I might be buying and/or selling the securities mentioned herein and/or its derivative at any time, regardless of (and possibly contrary to) the content of this blog post.

I undertake no responsibility to update my disclosures and they may therefore be inaccurate thereafter. Likewise, any opinions are as of the date of publication, and are subject to change without notice and may not be updated. I believe that the sources of information I use are accurate but there can be no assurance that they are. All investments carry the risk of loss and the securities mentioned herein may entail a high level of risk. Investors considering an investment should perform their own research and consult with a qualified investment professional.

I wrote this blog post myself, and it expresses my own opinions. I do not have a business relationship with any company whose stock is mentioned in this blog post. The information in this blog post is for informational purposes only and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

The primary purpose of this blog post is to share industry expertise and research and receive feedback (confirmation / refutation) regarding my investment theses.