/ July 13 / Weekly Preview

-

Monday:

N/A

---

Tuesday:

Core Inflation Rate YoY (2.9% exp.)

Inflation Rate YoY (3.9% exp.)

Fed Chair Warsh Testimony

---

Wednesday:

PPI MoM (0.2% exp.)

---

Thursday:

Retail Sales MoM (0.3% exp.)

Initial Jobless Claims (218K exp.)

---

Friday:

Housing Starts (1.33M exp.)

Michigan Consumer Sentiment Prel (51 exp.)

-

Monday:

N/A

---

Tuesday:

J P Morgan Chase & Co

Bank of America Corporation

Goldman Sachs Group, Inc. (The)

Wells Fargo & Company

Citigroup Inc.

---

Wednesday:

ASML Holding N.V.

Johnson & Johnson

Morgan Stanley

BlackRock, Inc.

---

Thursday:

Taiwan Semiconductor Manufacturing Company Ltd.

UnitedHealth Group Incorporated

Netflix, Inc.

Abbott Laboratories

---

Friday:

Regions Financial Corporation

Autoliv, Inc.

Bank Earnings Tell The Story

Got a question about the markets, your investments, or a topic you’d like us to discuss in an upcoming article? We read every message and may feature your question in our daily write-ups!

Email: andrei@signal-sigma.com

Follow & DM on X: @signal_sigma

Last week, the tape flipped in a way we had anticipated. Leadership was provided by mega-cap growth stocks which had been agressivley sold off due to AI CAPEX concerns. As a consequence, SPY rose +1.36% on the week and currently sits less than 1% below the June all-time-high. Similarly, the Nasdaq added +1.8%, powered by the same handful of stocks.

Meta took the spotlight with a +14.5% advance, with Nvidia also gaining +7.8% in an environment of semiconductor volatility. Contrasting these, the Dow slipped -0.3% and the Russell 2000 underperformed with a -0.53% loss. The Equally Weighted S&P 500 (RSP) also dipped -0.18%. The average stock went nowhere, while the benchmark indices were powered by the Mag 7 “generals”.

From a macro perspective, things are starting to get interesting due to a confluence of conflicting factors. June payrolls came in at 57K, roughly half of what economists expected. Soft labor data would be a warning normally, but the markets cheered this particular miss as it reinforced the probability of a September rate cut (or at least diminished the possibility of a hike).

A counterpoint to that thesis is hotter inflation that does not corroborate the outlook. This becomes especially valid, as oil climbs back up in the wake of a new geopolitical flare-up over the weekend. A slowing job market coupled with sticky inflation is not what the Fed wants to see.

Across Sectors, Energy (XLE) and Tech (XLK) were dominant (a rare setup), while defensives like Basic Materials (XLB) and Healthcare (XLV) and Staples (XLP) lagged badly.

The 10-year treasury yield ran back up to 4.59% from 4.49% a week earlier, in a sign the bond market is still evaluating the Fed’s rate approach. Meanwhile, the VIX finished at 15.03, in a sign of little demand for short term protection. A calm tape, cooling jobs and hot inflation cannot coexist for long.

This week, we’ll see whether the mega cap component can prove its durable leadership status or if last week was a head fake. In any case, the very high returns variance within the Mag 7 cohort persists, with investors opting to be highly discerning with their allocations. Previously, higher levels of variance within this group have been associated with a positive (if volatile) market backdrop.

Technically, we’re seeing SPY trading above both its 20 and 50-Day moving averages (both of which are sloping upward). This is an unambiguously bullish structure. The MACD signal is positive and so is our Buying Regime indicator.

From a support and resistance standpoint, the benchmark ETF is consolidating, unable so far to break either higher or lower from the current range. As such, the technical picture has not materially changed. Dark Pools investors have been relative buyers over the past week, with the caveat that overall exchange volume was relatively low. GEX is healthy and should keep a lid on volatility in the coming days.

Our only complaint is that the headline S&P 500 index price action was primarily driven by a handful of names, while the equal weighted and small caps components slipped. Dollar volume, especially in Tech, was underwhelming, with the push higher occuring on unremarkable participation.

For now, there is no evidence of a broader thrust that can reliably push the market to fresh all time highs. This is a setup that argues for discipline rather than taking on new risk. Buying on pullbacks offers higher odds of success than chasing breakouts at this juncture.

As the near term structure is range-bound rather than trending, we’re looking for the 50-DMA to hold as support. Failing that, the next important line in the sand becomes $728 (M-Trend).

Looking forward, the story of the week is two-fold, with Tuesday becoming the focal point. We’ll get the CPI report at 8:30 a.m, with economists looking for a cooler headline near 3.7% year over year. However, the Cleveland Fed nowcast is tracking closer to 4%, while real-time tracker Truflation is indicating a lower number, near 2%.

The gap between these estimates is the whole ballgame for the September hike / pause / cut decision at the Fed. A hot print at 4% would force the market to rapidly reprice Fed expectations, whereas a softer print around 3.5% would allow the September-cut narrative to persist.

PPI is released Wednesday, retail sales and jobless claims arrive Thursday, and Friday brings housing starts plus the preliminary July consumer sentiment reading. Any signs of persistent inflation alongside a weakening labor market will rekindle the market’s stagflation concerns.

On the earnings side, large banks open Q2 earnings season, with the focus on their commentary regarding credit and the consumer. Every quarter, the playbook is the same. The health of any bull market ultimately comes down to the underlying economy. Banks offer us a clean window into that economy, with the American consumer as the driving force. While headlines will be filled by investment-banking and trading revenues, the real story is in the credit signals.

We’re watching the following:

Loan loss provisions (higher means management is expecting more borrowers to fall behind)

Net charge-offs (higher means more loans have been written off as realized losses)

Card delinquencies (higher indicates stress on the consumer)

Loan growth (lower means that households and businesses are pulling back)

Deposits (cash balances indicate the cushion that consumers have)

The reason that these numbers matter is the job market. A consumer with a job can service debt. A consumer without a job cannot.

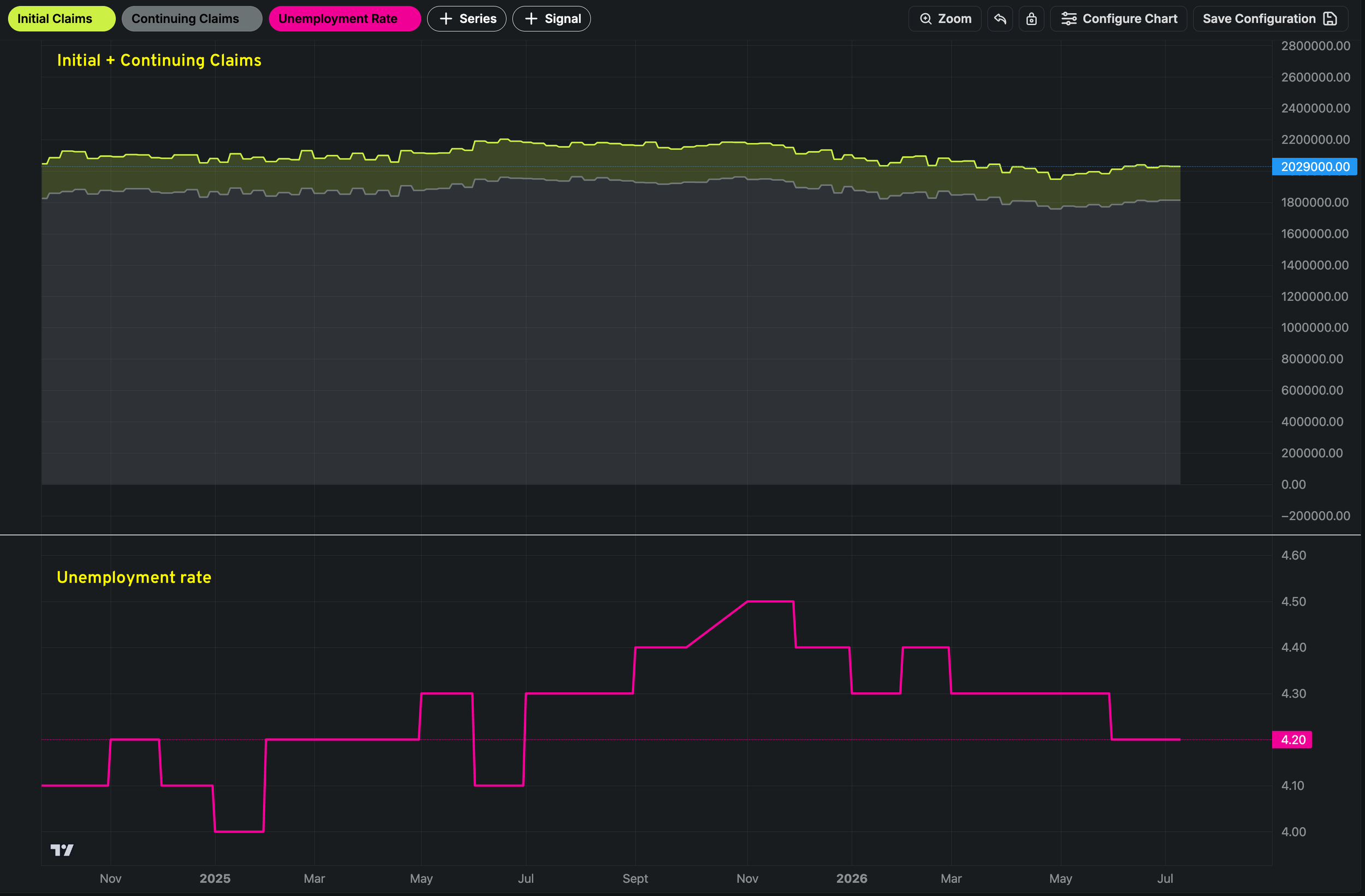

With June hiring at roughly half the expected rate, a rise in card delinquencies would indicate the jobs slowdown is already straining household balance sheets. Looking at the jobs market through the lens of Initial + Continuing claims alongside the official unemployment rate, we’re not seeing any immediate trouble. But data from the banks will paint a clearer picture weeks or even months before any official number hits the tape. After all, banks vote with their balance sheet, and a reserve buildup carries more information than any survey.

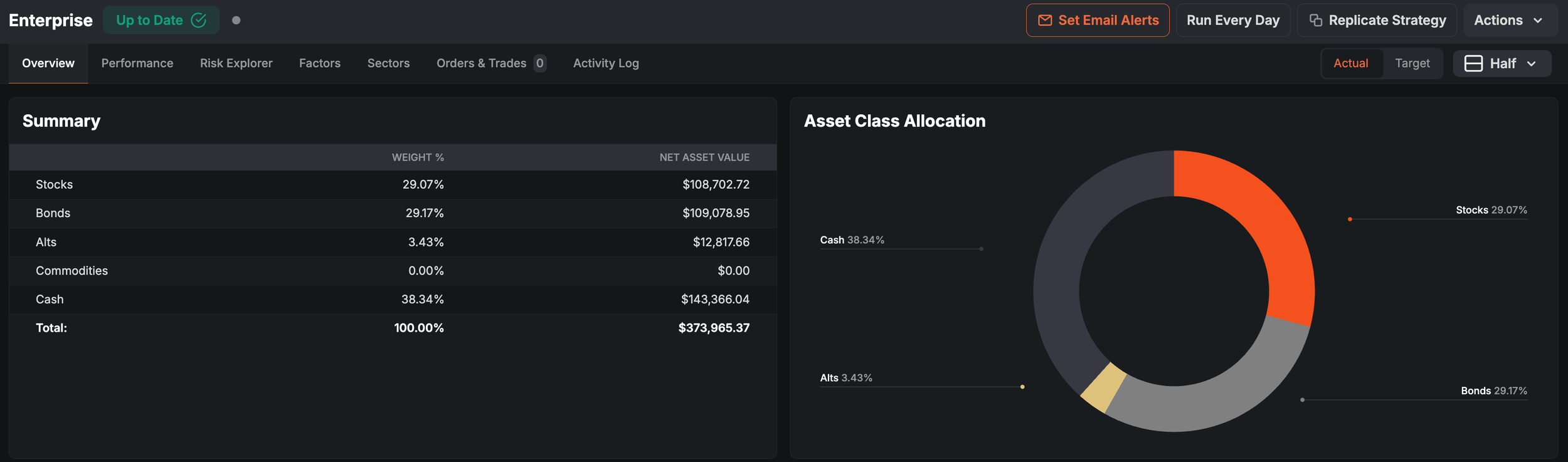

Geopolitics complicate the setup, as oil is set to rise +4% and futures are pointing to a firmly lower start of the week. Our Enterprise asset allocation model is currently playing defense, with a hefty 38% of its portfolio sitting in cash and just 29% equity risk (down from over 80% at the start of June).

Our Trading Strategy (Sigma Portfolio)

If the banks confirm a resilient consumer, this bull market can broaden back out. Similarly, if inflation trends lower, the market will breathe a sigh of relief.

Conversely, if reserve lines begin rising while inflation remains elevated, then the June jobs shortfall will have proved a serious warning. We’ll learn a lot by Tuesday’s market open, as both the CPI numbers and bank earnings hit the tape simultaneously.

While our live portfolio contains an increased dose of risk, we would be wary of chasing markets higher in the near term. In our client portfolios which are not yet fully allocated, we will be buyers on this most recent dip. The quarter ahead is notoriously volatile, as the summer months lack both liquidity and are seasonally weak (the range of Q3 outcomes over the past decade has been +12% / -10.6%).

Our read is that the market is not done with the current consolidation pattern and a rotation is still in the works. Put simply, we don’t have high hopes for stock market gains in the near term, but as long as support holds, a positive setup is forming for the end of the year.

Disclosures / Disclaimers: This is not a solicitation to buy, sell, or otherwise transact any stock or its derivatives. Nor should it be construed as an endorsement of any particular investment or opinion of the stock’s current or future price. To be clear, I do not encourage or recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the facts or perceived implications of this blog post. I currently do not own or plan to own any position, long or short, in the securities mentioned.

I am not a financial advisor licensed in the United States. Nor am I providing any recommendations, price targets, or opinions about valuation regarding the companies discussed herein. Any disclosures regarding my holdings are true as of the time this article is written, but subject to change without notice. I frequently trade my positions, often on an intraday basis. Thus, it is possible that I might be buying and/or selling the securities mentioned herein and/or its derivative at any time, regardless of (and possibly contrary to) the content of this blog post.

I undertake no responsibility to update my disclosures and they may therefore be inaccurate thereafter. Likewise, any opinions are as of the date of publication, and are subject to change without notice and may not be updated. I believe that the sources of information I use are accurate but there can be no assurance that they are. All investments carry the risk of loss and the securities mentioned herein may entail a high level of risk. Investors considering an investment should perform their own research and consult with a qualified investment professional.

I wrote this blog post myself, and it expresses my own opinions. I do not have a business relationship with any company whose stock is mentioned in this blog post. The information in this blog post is for informational purposes only and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

The primary purpose of this blog post is to share industry expertise and research and receive feedback (confirmation / refutation) regarding my investment theses.