/ February 16 / Weekly Preview

-

Monday:

Market Closed

---

Tuesday:

NY Empire State Manufacturing Index

---

Wednesday:

Building Permits Prel (1.4M exp)

Housing Starts (1.33M exp.)

FOMC Minutes

---

Thursday:

Initial Jobless Claims (225K exp.)

---

Friday:

Core PCE Price Index MoM (0.4% exp.)

GDP Growth Rate QoQ Adv (3% exp.)

Personal Income MoM (0.3% exp.)

Personal Spending MoM (0.4% exp.)

-

Monday:

N/A

---

Tuesday:

Palo Alto Networks, Inc.

Cadence Design Systems, Inc.

---

Wednesday:

HSBC Holdings plc

Analog Devices, Inc.

Booking Holdings Inc.

Carvana Co.

---

Thursday:

Walmart Inc.

Alibaba Group Holding Limited

Deere & Company

Southern Company (The)

---

Friday:

N/A

Tech Weakness Overdone?

Next week (23–28 February) we’ll be on winter break; only significant market developments will be covered on our blog.

Got a question about the markets, your investments, or a topic you’d like us to discuss in an upcoming article? We read every message and may feature your question in our daily write-ups!

Email: andrei@signal-sigma.com

Follow & DM on X: @signal_sigma

As we noted last week, February tends to be a weaker month in terms of returns. So far it has entirely lived up to statistical expectations, with a vicious rotation from growth to value hammering index-level performance.

SPY is slightly negative year to date, dragged lower by its heavy reliance on Mega-Caps (MGK - the worst performing factor in 2026). Gains have been recorded in mid and small caps especially + the equal weight version of the S&P 500 and the value factor (RSP & IVE). Energy, financials, and industrials continued to attract flows as investors leaned into cash flow, dividends, and near-term earnings certainty.

Simultaneously, capital rotated out of technology, and particularly software stocks. With Q4 Earnings Season winding down, it’s worth noting that fundamentals like valuations and growth rates don’t exactly line up with the recent price action. Let’s explore…

We have just finished work on a sector by sector Valuation Dashboard that breaks down the median price to sales for each S&P Sector. In this study, every tab shows the historical median range for the most representative stocks within its industry, providing context to evaluate both the overall market price and the prices of each key stock group.

The clear conclusion is that the median stock is highly valued, with only the post‑COVID highs exceeding current P/Sales levels.

However, Tech is not by far the leader that it once was. The average technology stock is trading near the midpoint of its historical range, with current valuations similar to those recorded in 2017 and 2019.

If there were any valuation concerns in the sector prior to the latest correction, now these should be all but put to rest. Tech is not yet cheap by any means, but multiples have compressed to reasonable levels.

Take a look at Basic Materials, however. While cheaper on an absolute basis than Tech, Basic Materials stocks are now trading with multiples near the upper end of the range relative to their own history.

While the sector (along with Industrials and Financials) may have better earnings “certainty,” the earnings growth rates don’t justify the recent valuation expansion.

Furthermore, according to FactSet, investors have been chasing weak-growth sectors of the economy in terms of revenue…

…while the very clear loser has been software, with the S&P 500 software and services group (IGV) lagging the S&P 500 by roughly 24% over the last 3 months. This is near the widest gap in decades.

The driver of this massive capital flow recently has been a “narrative” in which investors believe that AI will make all specialized software companies useless. This will most likely fail to materialize. Sure, some companies may fall victim to the AI transition wave, but these are the ones with smaller moats to begin with. Other large players will most likely adapt. Salesforce, Oracle, and ServiceNow, will embed AI into enterprise applications to deliver complementary value, expanding TAMs without becoming displaced themselves.

In our view, the software selloff is likely getting overdone (at least in the short term) and investors can start picking off opportunities at attractive prices.

Unsurprisingly, the options market is pricing in the most long-term upside relative to medium-term downside for software and communications stocks out of all Sectors ETFs.

From a fundamental perspective, the EPS growth that underpins high valuations in the S&P 500 is coming from the companies which have been punished by price action at the start of the year. Another way to put it - the price has moved faster than fundamentals, this time to the downside. Software stock valuations have only been cheaper in 2018, after the short-volatility trade blew up.

Aside from the sector rotation, there were two notable catalysts last week: labor and inflation.

Payrolls rose by 130,000 and the unemployment rate fell to 4.3%. Most of the employment gain was due to seasonal adjustments and is probably reflecting a substantially weaker labor market. Gains are likely to be revised away next month.

Inflation cooled to 2.4% YoY, with Fed rate cut expectations moving higher after the report. The bond market reacted positively to both data points, and the 10-year Treasury yield moved towards 4%.

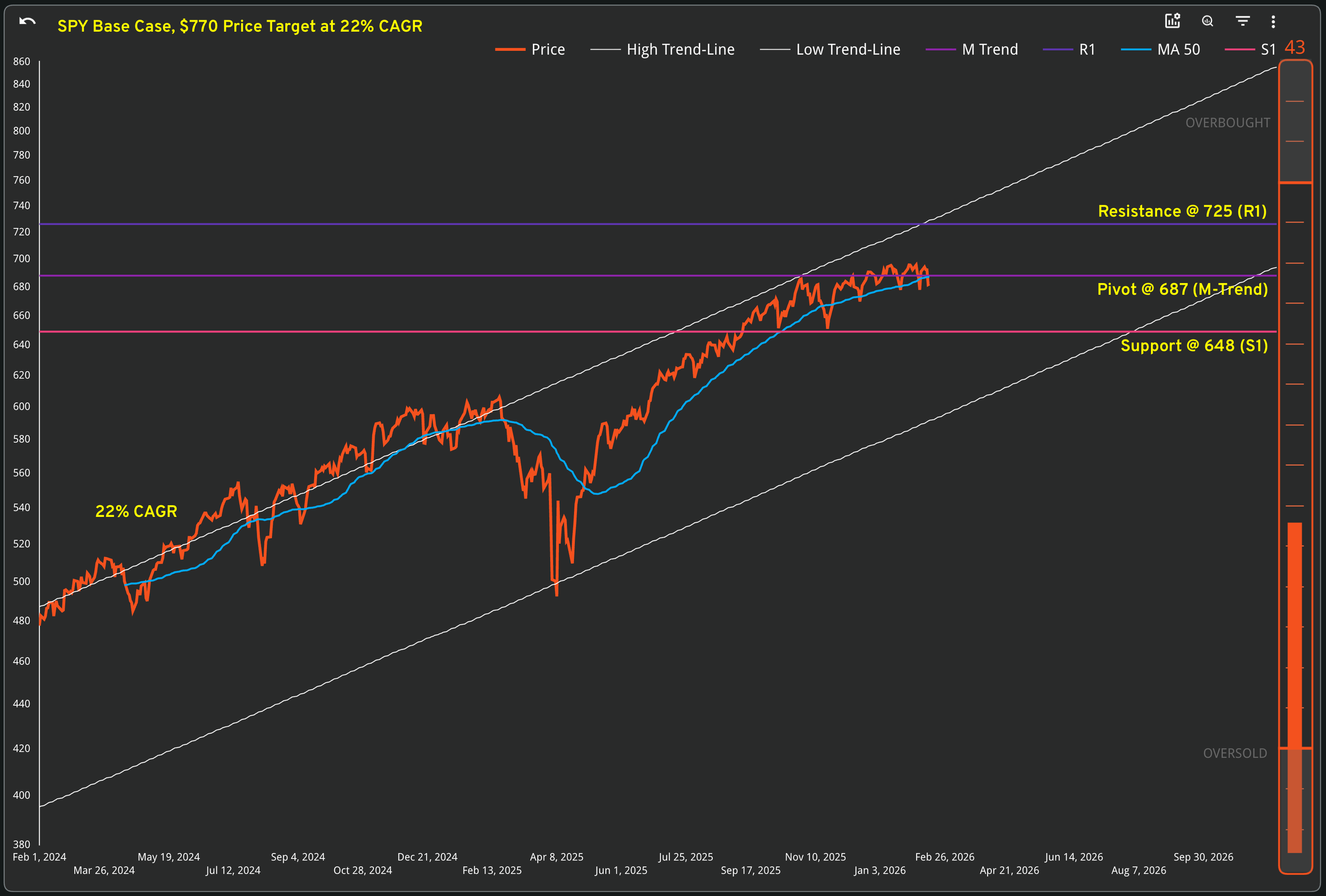

Technically speaking, the S&P 500 keeps failing near all-time-highs. The market has remained in a broad consolidation pattern since last October and February returns tend to be weak. Key support ($687) has been broken on Thursday, with near term weakness manifesting as negative GEX. Selling pressure was mostly contained in mega cap names, pulling the broader index lower. However, the growth > value rotation is getting extended here.

While volatility remains relatively contained, the market needs to reclaim $687 fast. If price fails there, rallies invite sellers, and the market may head lower, to $648 (S1). A break to the upside sets the stage for a rally to all-time highs and $725 afterwards.

Our Trading Strategy (Sigma Portfolio)

We have already reduced exposure and raised cash in anticipation of elevated volatility. Current conditions do not impose more drastic measures than this, and we may start picking off quality software stocks in the aftermath of the correction, using two of our ranking systems (Millennium Alpha and Vision).

The calendar this week starts with a market holiday, then the schedule picks up fast. investors receive the NY Empire State Manufacturing Survey and the NAHB Housing Market Index on Tuesday. There will also be Fed speakers. Our models will rebalance portfolios on Wednesday, when the housing market data hits the tape. If mortgage demand weakens again, the bond market tends to price a slower growth path.

Friday is the main event, with core / headline PCE, personal income / spending and Q4 GDP figures being published. Should core PCE pick up again, yields would likely rise, weighing on long-duration growth stocks. Conversely, if PCE eases while spending remains firm, the market sees a soft-landing scenario and bonds typically rally.

We’d like to see the market stabilize first and tech stocks put in a viable bottom. At the moment, there is enough fragility in stocks to become potentially problematic if key technical levels cannot be maintained. Again, the Enterprise model will prove key here.

Disclosures / Disclaimers: This is not a solicitation to buy, sell, or otherwise transact any stock or its derivatives. Nor should it be construed as an endorsement of any particular investment or opinion of the stock’s current or future price. To be clear, I do not encourage or recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the facts or perceived implications of this blog post. I currently do not own or plan to own any position, long or short, in the securities mentioned.

I am not a financial advisor licensed in the United States. Nor am I providing any recommendations, price targets, or opinions about valuation regarding the companies discussed herein. Any disclosures regarding my holdings are true as of the time this article is written, but subject to change without notice. I frequently trade my positions, often on an intraday basis. Thus, it is possible that I might be buying and/or selling the securities mentioned herein and/or its derivative at any time, regardless of (and possibly contrary to) the content of this blog post.

I undertake no responsibility to update my disclosures and they may therefore be inaccurate thereafter. Likewise, any opinions are as of the date of publication, and are subject to change without notice and may not be updated. I believe that the sources of information I use are accurate but there can be no assurance that they are. All investments carry the risk of loss and the securities mentioned herein may entail a high level of risk. Investors considering an investment should perform their own research and consult with a qualified investment professional.

I wrote this blog post myself, and it expresses my own opinions. I do not have a business relationship with any company whose stock is mentioned in this blog post. The information in this blog post is for informational purposes only and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

The primary purpose of this blog post is to share industry expertise and research and receive feedback (confirmation / refutation) regarding my investment theses.